𝗗𝗮𝗿𝗸 𝗣𝗮𝘁𝘁𝗲𝗿𝗻𝘀 𝗶𝗻 𝗧𝗿𝗮𝗱𝗶𝗻𝗴 𝗔𝗽𝗽𝘀

Consumer Protection Act guidelines on dark patterns have been around since 2023. Notices have been issued to high profile violators like Amazon and IndiGo, among others. Trading apps, unfortunately, haven't yet gotten the memo.

𝗙𝗼𝗿𝗰𝗲𝗱 𝗔𝗰𝘁𝗶𝗼𝗻

Nobody reads the checkboxes they tick during sign up. Most of the time, it doesn't matter. Sometimes, it does.

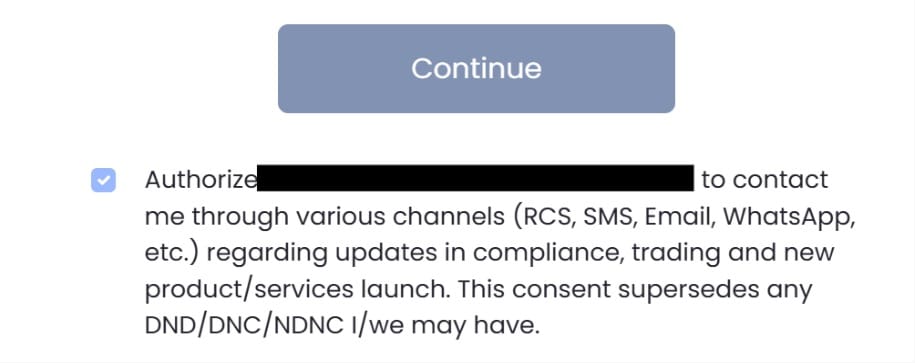

Here's one from a top 20 discount broker —

"Authorize xyz to contact me through various channels (RCS, SMS, Email, WhatsApp, etc.) regarding updates in compliance, trading and new product/services launch. This consent supersedes any DND/DNC/NDNC I/we may have."

You're signing away your right to not be contacted, bundled in with opening a trading account. You can't proceed without ticking it.

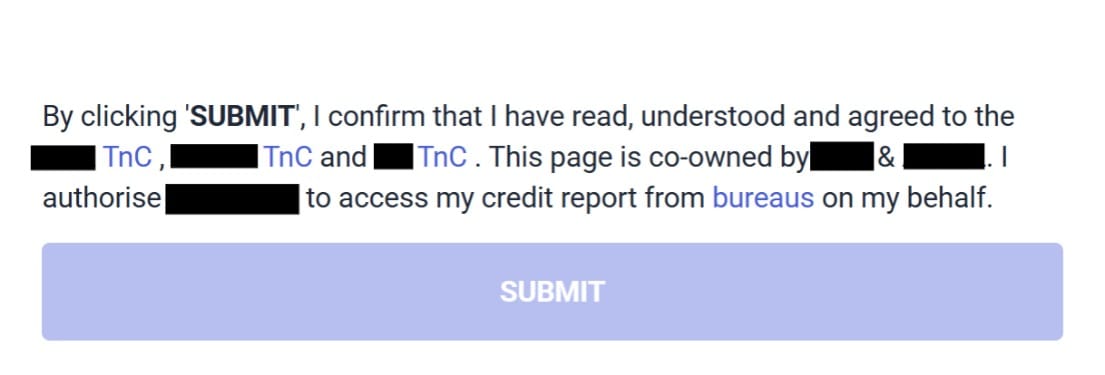

Here's another, from one of the top five largest brokers —

"By clicking SUBMIT, I confirm that I have read, understood and agreed to the xyz TnC, abc TnC and xxx TnC. This page is co-owned by abc & xyz."

One checkbox, two entities, the other being in a different line of business altogether. Your data is now shared across both of them, and you had no option to agree to one without the other. Expect a deluge of calls selling you insurance policies after you sign up with them.

𝗣𝗿𝗶𝗰𝗶𝗻𝗴 𝗣𝗮𝘁𝘁𝗲𝗿𝗻𝘀

Customers analyse broker pricing by comparing three things: account opening charges, annual maintenance, and brokerage. Brokers know this, so they've optimised these to be as close to zero as possible. The obvious question is: if a broker charges nothing for these three, how do they make money?

One of the largest banking brokers charges nothing on all three for youth under 30 years and API users accounting for a majority of the trades. The fine print is hidden in Depository Participant charges, levied at 0.04% or Rs 20, whichever is higher, every time you sell holdings. A sale of Rs 10 lakh means Rs 400 in DP charges. Rs 3.50 of that goes to NSDL. The rest is the broker's margin. Most customers don't even know DP charges exist, let alone compare them.

𝗡𝗮𝗴𝗴𝗶𝗻𝗴

The image is a classic. The options are "Allow" and "Later" instead of “Not Allow" or "No". There's no way to permanently decline, just an infinite loop of being asked again until you say yes.

𝗜𝗻𝘁𝗲𝗿𝗳𝗮𝗰𝗲 𝗜𝗻𝘁𝗲𝗿𝗳𝗲𝗿𝗲𝗻𝗰𝗲

Some trading apps open to a wall of content — trending stocks, loan offers, mutual fund recommendations, IPO listings — before you can get to what you came for. The argument is that it helps users explore. Maybe. But it should be opt-in, not the default landing experience. Particularly when what's being surfaced includes loans packaged as leverage, peer trading activity, and cross-sells for unrelated products.

While researching this piece, I realised we had a dark pattern of our own — our trading window defaulted to intraday. We've since changed it to long term. We eat our own cooking.